Why QR Still Wins in Malaysia (Even When Cards Are Everywhere)

Walk into almost any café, retail shop, or even a roadside stall in Malaysia, and you’ll notice something consistent. Right next to the counter, there’s a QR code. Sometimes more than one.

What’s interesting is that many of these places also accept cards. Contactless payments are widely available, terminals are more common than ever, and tapping a card is quick and easy. By most measures, cards should be enough.

And yet, QR isn’t going anywhere.

So the question isn’t whether QR is better technology. It’s why it continues to be the preferred option in so many situations, even when alternatives exist.

It fits how Malaysians already pay

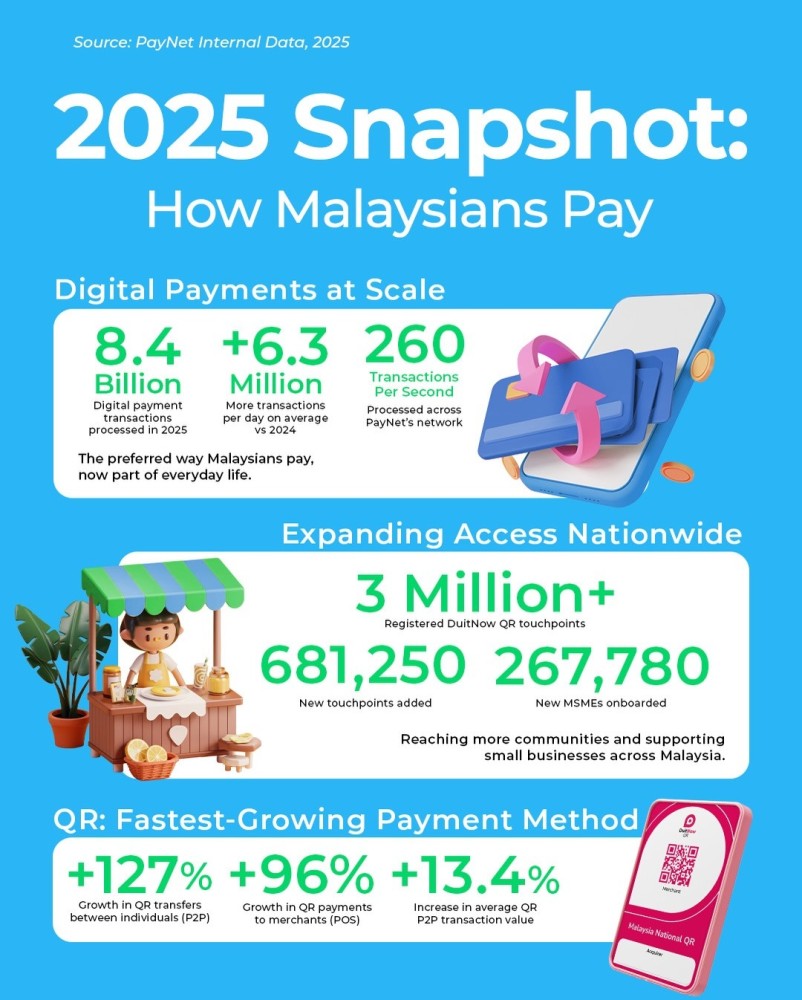

One of the simplest explanations is also the most overlooked. QR works because it fits into habits that are already there. According to Bank Negara Malaysia, digital payments per capita have increased significantly over the past decade, with over 90% of adults now using digital payment methods. (1)

Malaysia has seen rapid adoption of digital payments over the past few years, particularly through e-wallets. For many consumers, apps like Touch ’n Go, GrabPay, MAE, and Boost are already part of daily life. They are used not just for payments, but for transfers, rewards, and even basic financial management.

In that context, QR payments do not feel like a new behaviour. They feel like a natural extension of something users are already comfortable with. Open the app, scan, confirm, and move on.

There is also very little friction in that process. There is no need to reach for a wallet, no need to switch tools, and no uncertainty about whether the payment will work. That familiarity builds trust over time.

People rarely change payment habits unless they are forced to. In Malaysia, QR did not disrupt behaviour. It aligned with it.

It lowers the barrier for merchants

From the merchant’s perspective, the story is less about convenience and more about practicality. SMEs make up more than 97% of all businesses in Malaysia, which explains the need for simple and low-cost payment solutions. (2)

Accepting card payments typically involves some level of setup. There is hardware to consider, onboarding processes, and sometimes ongoing maintenance. For larger businesses, this is manageable. For smaller merchants, it can feel like a commitment.

QR removes most of that complexity. In many cases, it is as simple as generating a code and displaying it at the counter. There is no dependency on devices, no installation, and very little training required.

This matters in Malaysia, where SMEs make up the vast majority of businesses. Many operate with limited resources and prioritise solutions that are easy to adopt and easy to maintain.

For these merchants, QR is not just a payment method. It is an accessible entry point into digital payments.

That is a big reason why QR spread so quickly. It did not require merchants to change how they operate. It simply added a new option that fit into their existing setup.

Cost still plays a role

Cost is another factor that often sits in the background but influences decisions more than people realise.

Different payment methods come with different cost structures, and merchants are aware of this even if customers are not. For businesses with tight margins, especially in food and beverage or high-frequency retail, small differences in cost can have a noticeable impact over time. (3)

QR payments are often perceived as more manageable in this respect, particularly for smaller transactions. This makes them well suited for everyday purchases, where volume is high but individual transaction values are relatively low.

It is not that merchants are choosing QR over cards purely because of cost. It is that cost reinforces the decision when everything else already points in that direction.

In practice, merchants balance customer preference with business sustainability. QR happens to sit in a position that supports both.

It works beyond traditional retail

Another reason QR continues to perform well is its flexibility.

Card payments work best in structured environments where terminals are installed and maintained. But not every transaction happens in that kind of setting.

Malaysia has a diverse commercial landscape. Alongside malls and retail chains, there are night markets, roadside stalls, small service providers, and temporary setups that operate with minimal infrastructure.

In these environments, QR offers a simple solution. A printed code and a smartphone are enough to complete a transaction. There is no need to invest in hardware or worry about setup.

This allows QR to extend beyond traditional retail and into spaces where other payment methods are less practical. It becomes a universal option that works across both formal and informal settings.

That level of flexibility is difficult to replicate.

DuitNow QR made it even stronger

If there was one moment that pushed QR further into the mainstream in Malaysia, it was the introduction of DuitNow QR.

Before that, fragmentation was a real issue. Different wallets required different QR codes, and that created confusion for both merchants and customers. It also limited how widely a single setup could be used.

DuitNow QR addressed that problem by standardising the experience. One QR code could now accept payments from multiple banks and e-wallets. For merchants, this reduced complexity. For customers, it removed uncertainty. (4)

That standardisation made QR more reliable and easier to trust. It also encouraged wider adoption because the experience became consistent across different payment apps.

In many ways, DuitNow QR did not introduce QR to Malaysia. It made it scalable.

Speed is no longer the deciding factor

A common argument in favour of cards is speed. Contactless payments are quick, and in some cases, slightly faster than scanning a QR code.

But in reality, the difference is marginal.

For most transactions, especially in everyday retail environments, that difference does not meaningfully affect the customer experience. What matters more is how natural the process feels.

If someone is already using an e-wallet, scanning a QR code does not feel like an extra step. It feels like part of the same flow.

Speed matters, but only up to a point. Beyond that, familiarity and convenience tend to take over.

Cards are growing, just not replacing QR

None of this suggests that cards are losing relevance. In fact, card usage continues to grow, particularly for higher-value transactions and in more structured environments.

What is happening instead is coexistence.

Malaysia is not moving toward a single dominant payment method. It is evolving into a multi-method ecosystem where different options serve different purposes.

QR works well for flexible, everyday transactions. Cards remain strong in other areas. Both continue to grow, but in different ways.

It’s about fit, not dominance

QR did not succeed in Malaysia because it was the most advanced technology. It succeeded because it fits the way people live and the way businesses operate.

Payments evolve based on behaviour, economics, and environment. In Malaysia, QR sits at the intersection of all three.

Looking ahead, the focus is unlikely to be on replacing one method with another. Instead, it will be on enabling systems that support multiple payment types seamlessly.

For merchants, the challenge is not choosing between QR, cards, or e-wallets. It is managing them in a way that keeps operations simple and scalable.

Platforms like AmpersandPay help bring these payment methods together into a unified experience across channels, while infrastructure providers like CoherentPlus support the environments where these transactions happen.

Because in the end, the goal is not to decide which payment method wins.

It is to make payments work, quietly, in the background.

References

(1) Bank Negara Malaysia, Payment Statistics

(2) SME Corp Malaysia Report

(3) World Bank SME Digital Adoption Insights

(4) Payments Network Malaysia (PayNet), DuitNow QR Data